Tighter wheat, looser corn and soybeans

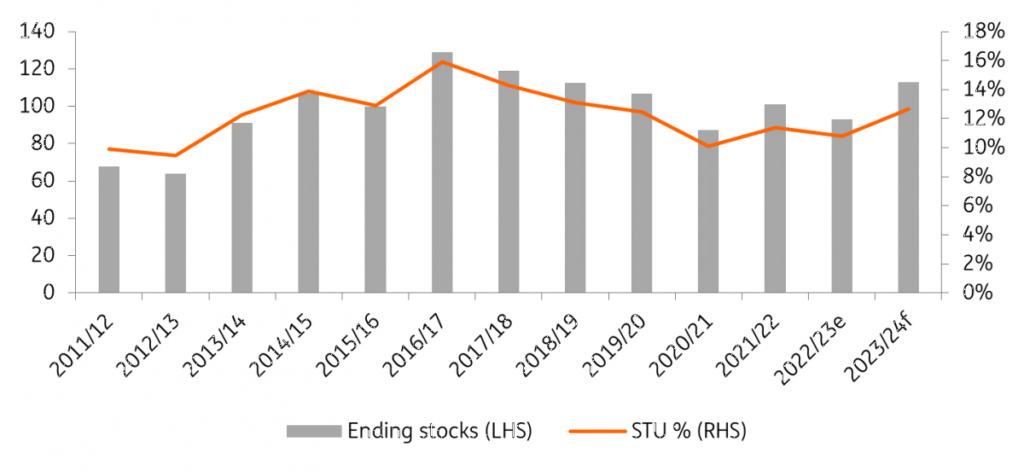

Global corn ending stocks grow in 2023/24.

Global ending stocks for 2023/24 are estimated at close to 315mn tonnes, an increase of almost 16mn tonnes year-on-year and the highest levels since 2018/19. Both the ex-China and US balance show a similar trend.

This is largely due to expectations that global corn output will grow by almost 64mn tonnes YoY. Supply increases from key producers have more than offset concerns over Ukrainian export supply. Meanwhile, weaker prices mean that global demand should rebound by a little over 3% in 2023/24, after declining by more than 1.5% the season before.

Supply dynamics suggest that corn prices are likely to remain under pressure for much of 2024 with prices needing to send a signal to farmers to reduce corn acreage.

US corn plantings to fall in 2024.

A key driver behind the increase in global output is the US, which is expected to produce a record crop of 15.24bn bushels (387mn tonnes) in 2023/24, an increase of 11% YoY. The increase has been driven by record acreage, whilst yield expectations have also improved as the season has developed.

However, with the 2023/24 US corn harvest largely complete, attention will be turning to 2024 plantings and what it means for the 2024/25 crop. The soybean/corn ratio in late 2024 (Nov’24 soybeans and Dec-24 corn), suggests that US farmers should increase soybean acreage at the expense of corn area.

We believe that planted corn acreage in 2024 could fall by around 4mn acres YoY to around 91mn acres. Yields in line with the five-year average would mean a US corn crop of 14.27bn bushels (363mt), down 6% YoY. This should still leave the US balance comfortable. However, obviously much will depend on how the weather plays out through the 2024 summer.

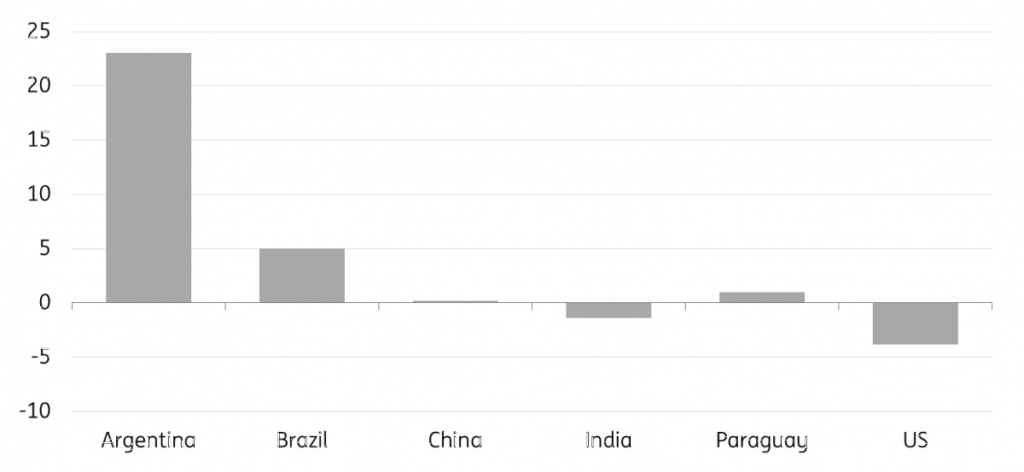

Argentina recovery adds to looser corn balance.

Expectations are that Argentina will see a recovery in its output in 2023/24 following last year’s drought. Argentine corn output is expected to increase by 21mn tonnes YoY to 55mn tonnes in 2023/24. Plantings for this crop are still underway.

Surprisingly, even Ukrainian output is estimated to have grown by 2.5mn tonnes YoY to 29.5mn tonnes in 2023/24. The weather has proved beneficial to yields, which has helped the crop. However, whilst Ukraine is seeing a larger harvest, this does not mean that additional supply will make its way onto the world market. The end of the Black Sea Grain Initiative has weighed heavily on Ukrainian grain exports. Therefore, if the war persists and there is no export deal, it is difficult to see a recovery in export volumes. As a result, we are likely to see a further buildup of stock in Ukraine, which could mean lower plantings and lower output in the upcoming season.

A region where we are set to see a fairly large decline in output is Brazil, where it is estimated that corn output will fall 8mn tonnes YoY to 129mn tonnes in 2023/24. Plantings are currently underway and weaker corn prices mean that farmers are expected to reduce plantings.

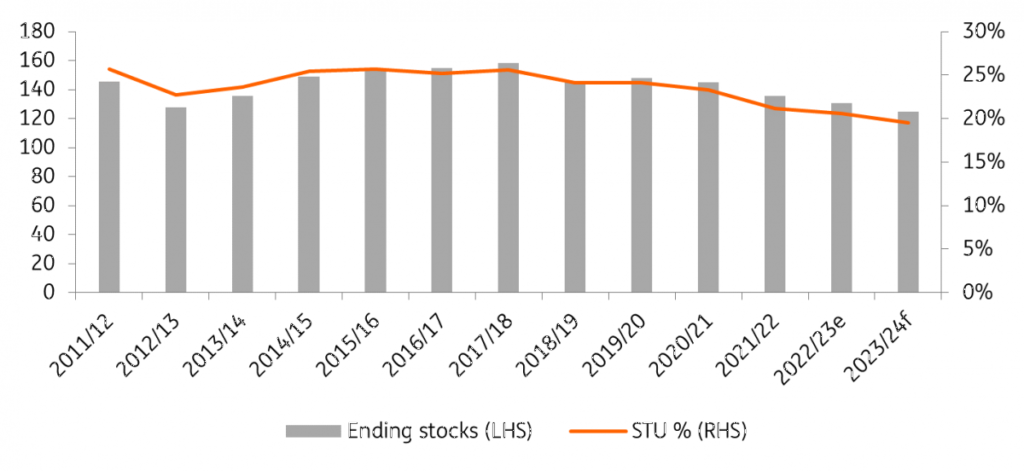

Wheat market set to tighten further.

The global wheat balance is set for another deficit through 2023/24. Global ending stocks are set to fall by 4% YoY to a little under 259mn tonnes, which will be the fourth consecutive season of declines in stock, leaving them at their lowest levels since 2015/16. However, a large amount of stock sits in China (52% of global). So, if we look at the ex-China balance, stocks are even tighter at less than 125mn tonnes, which is the lowest level since 2008/09. And if we look at the stocks-to-use (STU) ratio, to take into account the growth in consumption, the STU is 19.5%, the lowest since 2007/08.

While global ending stocks are set to edge lower this season, US wheat stocks are estimated grow by 10% to 1.8bn bushels (18.6mn tonnes) in 2023/24.

However, the tightening in the global balance (particularly the ex-China balance) suggests that wheat prices should be relatively better supported through 2024. We hold a moderately constructive view on wheat.

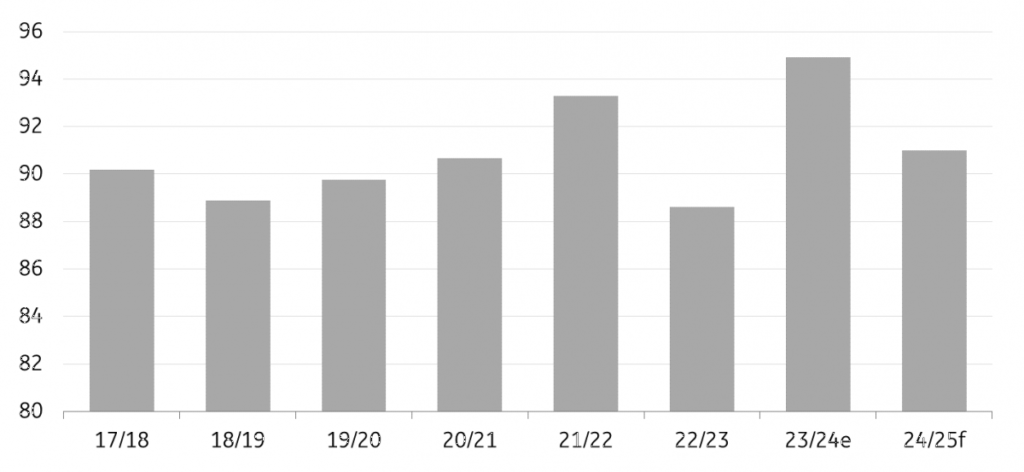

US wheat acreage to edge lower in 2024.

The US wheat market is relatively well supplied in 2023/24 with ending stocks edging higher over the course of the season. Higher acreage has helped to push the season’s crop to its highest levels since 2020/21. Still, while yields are also up from last season, they are quite a bit lower than levels seen between 2019/20 and 2021/22, particularly for hard red winter. However, higher acreage has offset lower-than-average yields.

Looking further ahead, winter wheat plantings for 2024 are already close to complete and the condition of the winter wheat crop is looking better than last year. While acreage is expected to decline by 3% in 2024, the current condition of winter wheat suggests that yields could be better YoY. Better yields and larger harvested area suggest that next season’s US wheat crop could be larger, despite a lower planted area.

Ukraine wheat output surprises to the upside.

The resilience of Ukraine’s agricultural sector has really stood out through the war. For the 2023/24 season, expectations were for the domestic wheat crop to fall on the back of lower acreage. However, yields have performed better than expected due to good precipitation and soil moisture, which has seen this season’s wheat crop grow a little less than 5% YoY to 22.5mn tonnes. This is also well above forecasts for a crop of less than 17mn tonnes earlier this year. However, as we have seen with most Ukrainian crops, the issue is the ability to export grain to the world market. As a result, we will likely see higher levels of stock carried in the domestic market. One would think this may lead to reduced plantings for 2024, however, Ukraine’s agricultural ministry estimates that planted area will likely be largely unchanged for next year.

Russian wheat output estimates creep higher.

A large part of the pressure on wheat prices this year has been driven by stronger-than-expected supply from Russia. Russia produced a record wheat crop of 92mn tonnes in 2022/23 and the expectation earlier in the year was for the 2023/24 crop to fall to a little less than 82mn tonnes. However, the crop has surprised and is estimated to total 90mn tonnes, the second-largest crop on record. As a result, Russia has retained its title as the largest wheat exporter and is expected to have record export supply of 50mn tonnes in 2023/24, up from 47.5mn tonnes last season. The recently announced grain export quota of 24mn tonnes for the period 15 February – 30 June 2024 should allow for another large export programme.

Australian wheat supply to fall in 2023/24.

Australia had three years of record wheat harvests through until 2022/23, with output totalling 39.7mn tonnes last season. Good rainfall and higher plantings helped with this record output. However, for 2023/24, the outlook is not as positive. Weather conditions have been drier, which should see yields fall from the record levels of more than 3t/ha last year to less than 2t/ha in 2023/24. These significantly lower yields and a 3% reduction in area mean that the Australian wheat harvest is estimated to fall 38% YoY to 24.5mn tonnes.

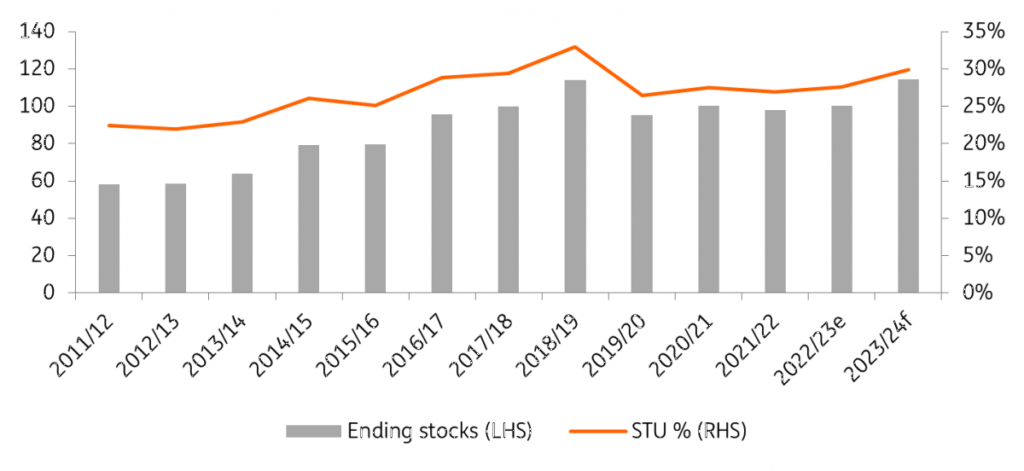

Global soybean stocks edge higher.

Despite soybean prices holding up relatively well this year, global ending stocks for 2023/24 are estimated to grow by more than 14% YoY to a record high of almost 115mn tonnes, which would leave the stocks-to-use ratio at close to 30%, also a record high. Expectations of higher ending stocks are being driven by the view that we will see strong output from South America in 2024.

While the global balance is set to loosen this season, the US balance is expected to tighten. US ending stocks are expected to fall a little more than 8% this year to 245mn bushels (6.7mn tonnes), the lowest levels since 2015/16. A smaller harvest this season and higher domestic crush is expected to tighten the market.

However, larger global stocks driven by stronger South American output and the expectation for larger US soybean acreage in 2024 suggest that prices will edge lower through 2024.

US soybean acreage to increase.

This season’s US soybean harvest is now complete, and it is estimated that farmers were able to produce 4.13bn bushels (a little more than 112mn tonnes), down around 3% YoY and the smallest crop since 2019/20. The reduction was largely due to reduced acreage, which fell from 87.5mn acres last season to 83.6mn acres this season.

While a smaller crop was harvested this season, domestic demand is estimated to be strong. In fact, demand is expected to hit record levels thanks to a stronger soybean crush. While crush margins have come off their highs, historically they are still at elevated levels. Soybean oil has played a big part in the broader strength in margins.

Looking at 2024 plantings, we expect that soybean acreage will increase. Soybean prices have held up relatively better than corn this year and the forward soybean/corn ratio suggests that farmers should increase soybean acreage at the expense of corn over 2024. Early estimates suggest that US soybean acreage could increase by 4% YoY to around 87mn acres. And if we were to assume average yields, that would result in a crop of almost 4.3bn bushels (117mn tonnes), up 3.9% YoY.

The ramping up of new crush capacity in the US this year and next suggests that domestic demand will grow next season. In fact, the growth in renewable diesel capacity in the US should continue to prove constructive for soybean demand in the years ahead.

As for export demand, given expectations for strong output from South America, US exports could come under some pressure, which should allow for ending stocks to still build next season.

Strong South American soybean output

South America is set to see strong output in 2023/24. Argentina is expected to see a recovery in output following the drought-hit crop of last season. Domestic production is forecast to grow 23mn tonnes YoY to 48mn tonnes.

As for Brazil, production is forecast to hit record levels for yet another season, with supply expected to grow by 5mn tonnes to 163mn tonnes in 2023/24. This growth is on the back of higher acreage, with soybeans relatively more attractive for farmers than corn. However, there are risks to this crop with dry conditions recently in some key growing regions, which could weigh somewhat on yields.

Strong Chinese soybean demand, but will it last?

China, the world’s largest soybean importer, has seen strong buying this year. Over the first 10 months of the year, imports totalled 82.4mn tonnes, up almost 15% YoY. And it appears as though strong imports will continue into early next year, with Chinese buyers recently booking large volumes of US soybeans for delivery into 1Q24. More recent buying appears to reflect stock building rather than actual consumption though.

Domestic demand fundamentals are weak. Chinese soybean crush margins are negative, whilst hog margins in China are also weak. This suggests that imports will also likely slow eventually, as weak hog margins will weigh on the pig herd size, which will ultimately weigh on feed demand.

Read also

Wheat in Southern Brazil Impacted by Dry Weather and Frosts

Oilseed Industry. Leaders and Strategies in the Times of a Great Change

Black Sea & Danube Region: Oilseed and Vegoil Markets Within Ongoing Transfor...

Serbia. The drought will cause extremely high losses for farmers this year

2023/24 Safrinha Corn in Brazil 91% Harvested

Got additional questions?

We will be happy to assist!

Write to us

Our manager will contact you soon