Brazil’s corn exports could see a 115% increase in 2022

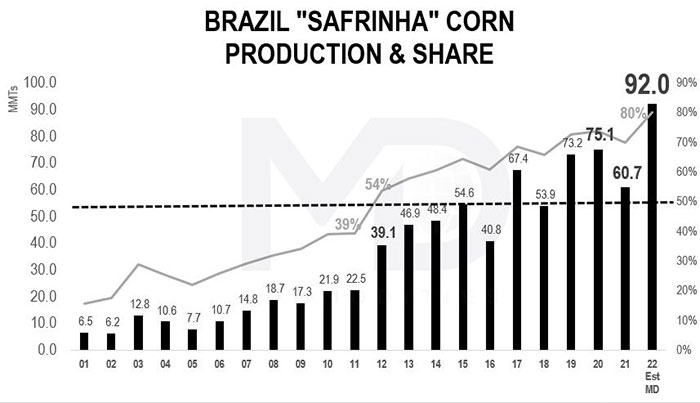

Most grain traders in the world know what that word refers to, but do you ever wonder where the name came from and why it has been adopted around the trade in its original form? Safrinha is an old name given to the country’s second or “winter” corn crop, meaning “small crop”. In the early 2000’s it represented as little as just under 20% of Brazil’s total corn production, hence the name “small crop”. That however is no longer true, by a large margin!

Brazil’s Safrinha surpassed the 50% share of production in Brazil in 2012, and never looked back. In its’ full potential, it now represents 80% of total Brazil production, a truly astounding number! Armed with know-how, technology and a blessed territory, Brazilian producers invested ever more in the Safrinha crop, making it what it is today, a true giant on its’ own right and largely responsible for the incredible story that is Brazil’s corn sector. The name remains Safrinha, but there is truly nothing small about it any longer…

On to 2022 and one of the best planting windows in history, along with nicely moist soils and a record area due to high prices all combine to put Brazil on the verge of record production & exports. Brazil’s Safrinha could reach as high 92-93 MMTs (with some estimates as high as 95 MMTs due to an aggressive increase in area). At 92 MMTs, “Safrinha” production alone could be around 5 MMTs higher than last year’s entire corn production, a potential 53% increase over last year’s drought ravaged 60 MMTs.

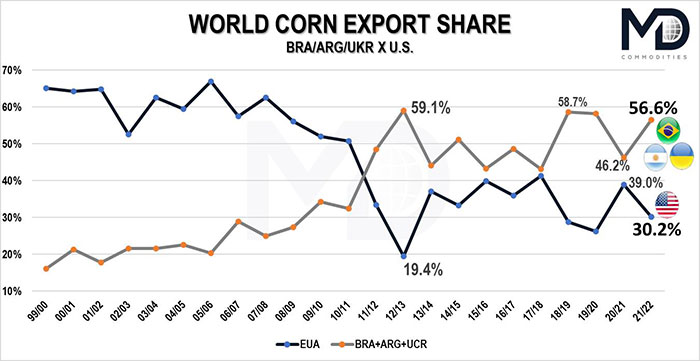

Of course, it is important to note that despite the wonderful start, nothing is guaranteed, as it will be March and early April weather that will dictate the fate of most of Brazil’s 2022 Safrinha. That being said, in case the production potential is at least mostly fulfilled with a Safrinha production close to 90 MMTs bringing the total corn crop near 115 MMTs (also a new record, 13 MMTs larger than 2020’s high), Brazil’s exports would be poised to shatter the old record of 40 MMTs, set in 2019. This year’s export potential is north of 43 MMTs, a number that would not only set a new record, but would again position Brazil atop the “Big Three” of Argentina, Ukraine and Brazil, three countries that together look to once again double the amount of corn the United States exports, as it did in 2019, and rebounding from last year’s poor performance vs the U.S. due to a multitude of factors, the main of which included the historical drought in Brazil that reduced the crop by around 25 MMTs!

Speaking of droughts, this year’s drought reduced (but still likely 2nd largest ever) soybean crop in Brazil will also play a role in enabling corn exports to potentially thrive starting in June/July. With less competition for exports especially after September, corn will have the full attention of Brazil’s export infrastructure.

The Big Three’s recent influence in world corn production and mainly exports cannot be understated. Argentina’s production growth has put it on the map as a consistent 30+ MMT exporter, with potential to soon export 40 MMTs consistently (weather permitting). Brazil’s domestic corn ethanol industry’s growth has skyrocketed in recent years, providing yet another incentive for continued investment in the grain in the country. MD Commodities estimates that by 2030 Brazil’s corn production could potentially climb to at least 140 MMTs, a number that would allow for consistent exports above 50 MMTs, bringing Brazil and the U.S. neck and neck to the finish, competing for the world’s leadership in exports. This was inconceivable even 10 years ago, and it could soon become a reality. Ukraine has rebounded very strongly in 21/22 with record production above 40 MMTs and exports over 30 MMTs. Combined, the Big Three could soon represent more than 70% of the world’s exports, up from around only 30% in 2010!

World corn markets are riding a wave of high speculative interest, providing historically high prices to producers worldwide. These prices are incentivizing production growth as in Brazil’s Safrinha this year and weather permitting will bring a lot of corn to world markets very soon. Will demand be high enough to counter such potential growth in production? The answer to that question and of course, performance of weather, will be determining factors for the fate of corn prices in the second half of 2022. It is also worth remembering that funds/investors/speculators currently hold a near record long position in corn futures, adding an incredible amount of premium into prices… how long they will ride that wave, no one knows, but what we do know is that when they decide to “abandon ship” the outcome for prices is not necessarily the best.

Read also

Wheat in Southern Brazil Impacted by Dry Weather and Frosts

Oilseed Industry. Leaders and Strategies in the Times of a Great Change

Black Sea & Danube Region: Oilseed and Vegoil Markets Within Ongoing Transfor...

Serbia. The drought will cause extremely high losses for farmers this year

2023/24 Safrinha Corn in Brazil 91% Harvested

Got additional questions?

We will be happy to assist!

Write to us

Our manager will contact you soon